Quit Your Job, Grow Your Startup

Working corporate from 9-5pm and startup business from 5-2am. It is not easy but you will make progress. After all work is work and you are doing something, which is always better then nothing. But, you will be distracted. Your startup business will not have your full attention and for that it will suffer. There is an answer though. Quit your job and focus on your startup. Here are some thoughts on just that.

Working corporate from 9-5pm and startup business from 5-2am. It is not easy but you will make progress. After all work is work and you are doing something, which is always better then nothing. But, you will be distracted. Your startup business will not have your full attention and for that it will suffer. There is an answer though. Quit your job and focus on your startup. Here are some thoughts on doing just that.

1. You Need to Raise Capital

Adeo Ressi, CEO of the Founder Institute says “It's important to quit your day job. I recently got an update from a graduate. Their company failed to raise capital and his day job was getting harder, so he had to close his startup. This comes as no surprise, since I have never heard of any startup that was able to raise professional angel money while the Founder was still employed. Furthermore, it's nearly impossible to dedicate the time and mental energy necessary to gain traction in the marketplace for your product while working for another company."

2. Quitting Your Job Is The Next Step to Success

Mohamed Kamal, Co-Founder and Head of Product for Gigturn adds, “Adeo is completely right. I bombed two investors meetings because I had a day job. Here’s the cold truth: Deciding you want to quit is usually just the first move in a long and cerebral chess match you’ll play with yourself. I’ve found that a founder's inability to quit their current day jobs had little to do with the perceived riskiness of their new startups, their financial situation, or general economic conditions. The real barrier for most of us is not external. It’s our own psychology – we:

- Overthink decisions

- Fear eventual failure

- Prioritize near-term, visible rewards over long-range success.

I found myself hesitating in front of an email send button. It was my resignation email which took three hours to write. Sending it was the ultimate mind hack."

3. There's No Such Thing as "Perfect Timing"

“My experience was similar, but with an extra ingredient... when I was about to quit my job my wife was diagnosed with cancer so it was an even harder decision. I talked to one of my advisors and he asked me, ‘When do you think it's the perfect time to start your company? There will always be a problem out there, you just have to choose if you want to do it or not.’ I then talked back to my wife and asked her if she would support me in case I didn’t raise enough money to live for a year and she agreed.

Now she has no cancer, we are about to receive new funds and the business looks promising. If I hadn't taken that decision in that apparently insane moment, none of this would be happening, so I really appreciate her faith in the project and the words from my advisor." - Sebastian Wilson, CEO at Luminux.cl.

4. Minimize Distractions to Reduce Mistakes

Tom Walpole, Co-Founder of Wembli, says “I have a meeting in about 3 hrs today to tell my employer I intend to focus on my startup full time. It’s a mind hack! In our situation, my co-founder happens to be my wife (they say co-founding is a marriage anyway right?!) - arriving at the decision that this is not only best for our business but also our family has definitely been a challenge, but at the same time a good measure of our ability to work as a team (in life and business) as well as an exercise in trust and support for each other.

I've spent the last 18 months developing, collecting user feedback and then developing again. Although that cycle never ends, it has come to a head where we have a refined enough product to start spending serious marketing money to grow it makes sense to us that we should minimize distractions which will hopefully reduce our mistakes and get more for our money.”

5. Part-Time Work May be a Better Option

“Whilst I was in FI I quit my day job to focus on my startup. It was the right decision. In order to fund day to day living I was just going off savings but I've also been fortunate in picking up some part time consultancy gigs which is a bonus. By consulting to the right companies I've also been exposed to some other contacts including investors so that's good too. Up until the product was available (in my case) the consultancy has worked great. Now that the site is live my work is cut out for me as I hustle away the plan is to focus on Oddswop and fundraising." - Yvonne Lee, Founder of Oddswop.

6. You Fail Faster

"The thing about having a job is that you don’t have the ability to fail fast. An unemployed founder has the entire day to meet partners and customers but an employed founder only has a few hours per day after work. And that’s assuming that people actually want to talk to you after working hours, instead of spending it with their families.

An unemployed founder has a fixed amount of money, so that forces the founder to really focus on being cost efficient. An employed founder, however, has a steady monthly salary so naturally it’s harder to focus because that founder can literally afford to do so. That means that what takes an unemployed founder 2 weeks to learn may very well take an employed founder 2 months. Compound that and you may end up spending years of your life on something that doesn’t work." - Elisha Tan, Founder of Learnemy.

7. You have to Constantly Deliver

According to Goran Candrlic, Co-Founder of Webiny: "We are scaling our product and team by doing consulting jobs. It's easier but it's constantly selling and delivering. So far we're alive and getting our core business up and running day by day."

8. The Devil's Advocate

Ramzi Zahra, Founder of Service List had some counter points to offer though. "I'd agree with the quit your job sooner then later theory however there are a few important matters to factor-in that are often forgotten. We can all agree that without putting the effort in a startup then it is likely that it will fail so you have a few choices:

1. Do it slow - Work on your start-up part-time/casually whilst keeping your day job.

2. Do it fast - Quit your day job to work on your startup.

An innate nature in humans is rush, they want results and they want it now. However to make the best decision it will depend on the grad's situation:

a. Stage of the startup - Early stage work is different than traction, funding, etc.

b. Financial situation - Can the founder afford to live without funding for a while?

I believe it is vital to factor the two points above to get the answer that is best for each situation. The second point is really critical. I personally quit my job to work on a startup however I soon found myself distracted with having to get some money in the door to pay rent/food/expenses. The startup was not "officially" launched yet and I was no where near raising funding. I chose to do some web development on the side to get by however it took a fair bit of time of my day. So did I really "quit" my day job? Some might argue that I didn't. In summary, Adeo's point is spot on however it cannot be used as a blanket rule and is more geared towards founders that are ready for funding."

Casey Neistat's Startup Lesson

If you know Casey Neistat then you know in 2015 he has started doing a vlog a day. In vlog #112 Casey shares his new startup story about BeMe Inc and how he was in the middle of fundraising at the same time his child was being born.

If you know Casey Neistat then you know in 2015 he has started doing a vlog a day. In vlog #112 Casey shares his new startup story about BeMe Inc. and how he was in the middle of fundraising at the same time his child was being born. Check it out below and in my opinion if you want to consume the most important piece of advice Casey gives, go ahead and skip to 2 minutes 10 seconds.

The only thing in life that stands between you and everything you have ever wanted to do, is doing it - Casey Neistat

What Makes a Successful Entrepreneur? Circumstance, Genetics, and Perseverance

Recently Adeo Ressi, Founder of the Founder Institute, was asked, “what does it take to be a successful entrepreneur?”. In Adeo’s opinion, his answer was successful entrepreneurship is a combination of three things: Genetics, Circumstance & Perseverance.

Steve Jobs

Recently Adeo Ressi, Founder of the Founder Institute, was asked, “what does it take to be a successful entrepreneur?”.

In Adeo’s opinion, his answer was successful entrepreneurship is a combination of three things: Genetics, Circumstance & Perseverance.

Let’s go through all three.

Adeo Ressi

1. Genetics

The Founder Institute has completed social science testing on over ten thousand prospective entrepreneurs, measuring things like “Big 5 Personality Traits”, Fluid Intelligence, IQ, and more. The Institute then watched who became successful, and correlated back the measured traits that best predicted success, in a scientific process.

The traits that best predict entrepreneurial success are genetic, such as Fluid Intelligence and Openness. BUT, just because you have traits that MAY make you successful as an entrepreneur, does not mean that you WILL be successful. Similarly, just because you are tall does not mean that you are good basketball player.

In other words, you need the raw materials, but you also need other things.

2. Circumstance

Being in the proverbial “right place at the right time” matters a lot towards your ultimate success as an entrepreneur.

Timing is everything (..almost).

For example, Michael Diamant started iClips, a site exactly like YouTube, a few years before YouTube launched. iClips was a truly well-executed business, but the necessary bandwidth, camera penetration, and streaming technology adoption did not yet exist for it to gain massive traction. He was simply too early for the market.

Circumstances are not all market-specific, either. You can have perfect market-timing, but your personal circumstances might not be optimal. For example, you could have the best idea and timing while you are a high school student, and start to execute on that idea to the the best of your ability — but then a veteran entrepreneur does the same business with millions in venture capital and captures the whole market.

Some circumstances are in your control, and some are simply outside of your control, but most successful entrepreneurs will concede that some of their success is attributable to circumstance.

3. Perservance

You only fail in your business when you actually give up, so, in fact, no business would ever fail if people persevered.

When you look at the Founders of some of the most successful technology companies in the world, and there almost always were (and still are) times when the Founders simply refused to give up despite unbelievable problems, stress, and negative signaling

“Entrepreneurship is like eating glass and walking on hot coals at the same time” — Elon Musk

Elon Musk

An entrepreneur faces all of the debilitating problems of their own life, coupled with all of the personal problems of their team, as well as hostile operating environments, limited capital, stretched resources, no time, regulatory burdens, changing technology… the list is endless.

The loneliness and darkness of entrepreneurship is not discussed very often, but it is very, very real.

Those that persevere succeed. Those that do not, do not.

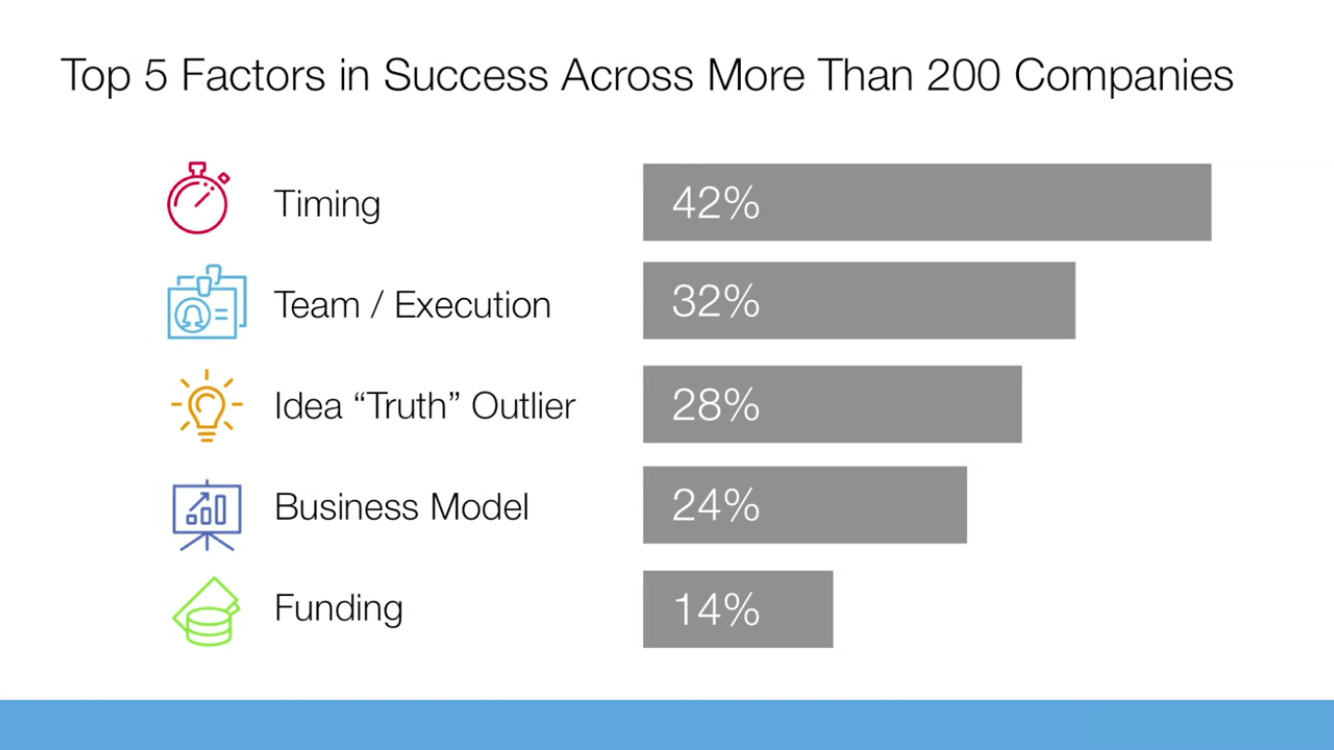

The Single Biggest Reason Why Startups Succeed

I was recently watching Charlie Kim, founder and CEO of Next Jump, presenting at the Founder Institute. During his talk he cited a TED talk by Bill Gross titled "The Single Biggest Reason Why Startups Succeed".

I was recently watching Charlie Kim, founder and CEO of Next Jump, presenting at the Founder Institute. During his talk he cited a TED talk by Bill Gross titled "The Single Biggest Reason Why Startups Succeed". I found the talk and enjoyed it so much I thought I would share it. You can find the link to it by clicking here.

Bill wanted to find out what is the single biggest reason startups succeed. He analyzed 200 companies. For each company he looked at the business traits of Funding, Business Model, Idea, Team, and Timing to determine which traits correlated most to its success. The quick synopsis is that the Bill Gross study showed that Timing (42%) is the single most important factor in a why a startup succeeds. Followed by Team (32%), Idea (28%), Business Model (24%), and lastly Funding at (14%).

What do you think? Agree? Disagree? Let me know in the comments below.

Why You Should Tell Everyone Your Startup Idea

Entrepreneurship is hard. Really hard. But with countless tales of how entrepreneurs made it big with almost nothing, it's easy for a budding founder to jump into the startup world full of unbridled enthusiasm and some startup misconceptions.

Entrepreneurship is hard. Really hard. But with countless tales of how entrepreneurs made it big with almost nothing, it's easy for a budding founder to jump into the startup world full of unbridled enthusiasm and some startup misconceptions.

As Director of the Founder Institute in New York one of the more common misconceptions I encounter with a lot aspiring entrepreneurs is that they are afraid of telling others their idea. There are numerous reasons though why entrepreneurs should share their startup ideas. While it is common among founders to be hesitant about divulging their startup secrets, the truth of the matter is that your company can benefit greatly from telling people what your idea is about and what you hope to achieve.

Myth #1: "I Should Save My Startup Idea Until It's Refined"

Reality: You should share your idea with everyone you meet. If you plan on pitching your idea to potential investors, why not practice beforehand? By sharing your idea with as many people as possible, you can get feedback early on to prevent wasting time on an idea that won't sell. In a Courtney Seiter-penned article titled Why No One Will Steal Your Startup Idea, Buffer CEO and Co-Founder Joel Gascoigne says:

"When you build a startup, you're basically creating something that doesn't exist already. In order to figure out if your idea is actually going to work, it's essential that you share it with people. You're going to have to do it sooner or later. The longer you leave it, the more risk there is that you spend a long time working on it, and then eventually you put it out there and find out it's not something that resonates."

Myth #2: "My Startup Idea Is Too Unique To Be Shared"

Reality: No, it's not. Just look at the countless companies that offer the same product. If you have an idea for a startup, there's a very good chance that there are a multitude of other entrepreneurs working on the exact same concept. But don't let that deter you, as you should focus less on the idea itself and more on how you plan to execute it. Here's what Cory Levy, Co-Founder at One, Inc., had to say in a Linkedin article titled Startup Secrets: Should I Hide My Business Idea?:

"Ideas are a dime a dozen; it's the execution that will set you apart from the rest. Chances are that there are people developing the same thing that you're working on now. We plan to compete not by keeping our idea secret, but by building the best possible team and by creating the best solution to the problem we are solving."

Myth #3: "People Will Steal My Startup Idea If I Tell Them What It Is"

Reality: Most likely not. The chances of someone stealing your idea are pretty slim. In fact, sharing your idea with others is a great way to drum up interest in your company and makes getting help easier. Still not convinced? Here's what serial entrepreneur Alexander Muse has to say in a Startup Muse article titled Should you share your idea?:

"If you keep your ideas a secret it will be impossible for anyone to actually help you. Could someone steal your idea? Of course, but as I've said before your potential competitors are more likely to become partners. You're far more passionate about your idea that anyone else - and most people want to partner with people with passion."

If you're still reticent about sharing your idea with others, take into account the multitude of opportunities that your company can benefit from by simply divulging what it is you do and how you're going to do it. And remember:

"If someone does take your idea, they will never have the passion you have for it because they didn't come up with it." - Joel Gascoigne

Entrepreneurial Spirit Is Driving Buffalo Forward

In recent years, much has been made about how the entrepreneurial movement is modernizing the American dream. Markets like San Francisco and New York City are home to some of the world's most recognizable startup success stories.

In recent years, much has been made about how the entrepreneurial movement is modernizing the American dream. Markets like San Francisco and New York City are home to some of the world's most recognizable startup success stories. And with good reason - being the top dog in a competitive market brings with it the advantages of recruiting top talent, visible press, and the ability to raise the innovative bar. But as billion dollar companies set up shop in big markets, a new generation of innovators is turning to midmarket cities to incubate their bold ideas. Cities like Buffalo, NY are making this possible. Buffalo is channeling its legacy of hard work - dating back to its heyday as a turn-of-the-twentieth-century giant - into a new push for entrepreneurial progress. Satish K. Tripathi, co-chair of the Western New York Regional Economic Development Council, and President of the University at Buffalo, perhaps said it best. The city is "open for business."

Taking a step back, Buffalo's innovative future is rooted in its time-tested work ethic. Last December, I reposted a video that discussed Buffalo as a city of firsts. From Frank Lloyd Wright to Theodore Roosevelt, the city boasts an impressive list of big thinkers with lasting impact. Of course, the city has experienced more than its fair share of setbacks. Following the 1950s opening of the Saint Lawrence Seaway, shipping and other industries moved elsewhere, businesses went vacant, and population decreased.

But today a number of trends indicate that the city is positioned for an entrepreneurial resurgence.

- A New Youth Movement - According to census data analyzed by the New York Times, from 2000 to 2012 the number of college graduates (ages 25-34) in Buffalo jumped 34 percent - more than Los Angeles, New York, Chicago, or even Boston.

- An Attractive Business Destination - A number of factors including access to an international border, a strong labor force, and low operations cost are gaining attention. Elon Musk's SolarCity made headlines last September with its announcement to commit 5 billion in Buffalo, while creating 3,000 new jobs. Beyond U.S. borders, a growing number of Canadian companies are also investing, leading to an even stronger startup corridor in the Golden Horseshoe - the densely populated region on the west end of Lake Ontario, stretching from Buffalo to Toronto .

- Renewed Sports Franchises - Not to be overlooked, Buffalo is also attracting new talent on the football field and in the hockey rink. The Bills and Sabres - arguably pivotal economic and emotional heartbeats of the city - are sporting new leadership with owners Terry and Kim Pegula and with the recent head coach hires of Rex Ryan and Dan Bylsma.

Within this movement, a number of newer companies face challenges of raising capital. To address this, organizations like 43North are incentivizing companies from around the world to incubate their ideas in Buffalo - with the potential to win up to $1 million. With support from New York State Governor Andrew Cuomo's Buffalo Billion initiative and the New York Power Authority, there is heavy commitment and high stakes in the organization, which last year received registrations from 96 countries and 50 states. The 11 winners from 2014 now share space in a new incubator at Buffalo Niagara Medical Center - specifically created to engage a collaborative entrepreneurial community.

As they wrap up registration this month, 43North wants to continue the momentum by focusing on quality global registrants to attract the best ideas the world over. This concept of exacting change through entrepreneurism is what's driving Buffalo forward. It's a bold venture for a city to bet on bright ideas and put them into action. But it's a critical step, with potentially high reward, in restoring the brightness to America's City of Light.

10 Rules for a Great Startup Idea

Even though it’s trendy in startups to say that ideas mean nothing and execution means everything, the reality is much less binary and much more nuanced. For example, even the world’s best entrepreneur with

Even though it’s trendy in startups to say that ideas mean nothing and execution means everything, the reality is much less binary and much more nuanced. For example, even the world’s best entrepreneur with incredible execution will fail if their idea is fundamentally flawed, or if their market is too small. This list of 10 rules put together by the Founder Institute aims to provide a great starting point for people who want to evaluate their startup ideas at the very first stage.

What we have found is that if an early-stage founder can check off the ten items below, they have a solid foundation by which to start a company. You are absolutely not assured success if you can check off these items (nor are you assured failure if you can’t), but your chances of success are much, much higher if you can.

1. You are a Passionate About It

Money is no substitute for passion, so every entrepreneurial journey should start with a passion. In fact, every aspiring founder who comes into the Founder Institute with a goal to just “flip” their company is advised to drop out during the first week for a full refund. There are two reasons for this;

In order to power through the hard times of being an entrepreneur, founders need to be working on ideas that they can see themselves still working on in 5, 10, or even 20 years. As Elon Musk famously said, “Being an entrepreneur is like eating glass and staring into the abyss of death.” If you don’t have the requisite passion, your chances of seeing a project through are minimal.

Other people will easily be able to see through your lack of passion, like customers, investors, and press. For example, investors are typically concerned more about the “why you”, then they are about the “why” of your idea.

2. It’s Simple

“Think big” is a common mantra for entrepreneurs. And it is true — every entrepreneur should think big, because in most cases, starting a company with small ambitions can be just as much work as one with big ambitions. However, most people confuse the “think big” mentality into meaning they have to try and “boil the ocean” from the outset.

Big ideas are raised, not born, and they are most often raised by simple pain points. For example, Mark Zuckerberg didn’t wake up one morning and say, “I’m am going to create the social graph.” Instead, he set out to build a simple utility for Harvard students to see who was in their classes.

All the great businesses of our time have started with an incredibly simple idea, and then expanded upon that. If you can start by solving one problem, with one product, for one customer, you will be sufficiently focused and can have a great foundation for success.

3. One Revenue Stream

For some reason, the majority of early-stage entrepreneurs think that the more revenue streams their idea can support, the better. In the early stage, you need to be laser-focused on one revenue stream, and your idea needs to have a clear, singular revenue stream that can conceivably be large enough to support the entire business. If not, then its time to go back to the drawing board.

Also, it’s a common misconception that companies who focused on early user growth (ex. Google) didn’t have a revenue model in mind when they started. In reality, these businesses saw incredible early traction, and then the founders made a tactical decision to shift their focus to growth.

Can someone build a great company with a zero revenue mentality from the outset? Sure. But building a business with no revenue stream in the hopes of becoming the next Instagram is like buying a lottery ticket — except that lottery ticket costs a lot more time and effort than $3.

4. Few Steps to Revenue

The more steps there are to revenue, the more complex an idea is to build out and execute.

This is a very important step during the ideation process: what are the things that need to happen before you make a dollar? If you have to provide a service in order to collect data that will then be sold to advertisers, for example, you have a very complex business. That would be 5+ steps to revenue. Try to limit the number of steps to revenue to around three from the beginning.

5. You Know the Customer

You need to understand very clearly who you are helping, what exactly they need, why they need it, how they would be willing to solve their problem, what they spend their money on, what goals they have in life… in other words, you need to have a very specific archetype.

A common mistake we encounter is that people don’t go nearly deep enough in their customer definition, or customer development. For example, many people will stop at “I am helping large companies hire.” In reality, they need to be able to say something like; “I am helping senior hiring managers at enterprise software companies in the United States with 400–800 employees. They are typically female, age 29–34, making an average of $58,000 per year. They report to the company HR lead, and their KPIs are X, Y, and Z, measured quarterly. They spend the majority of their day doing A, B, and C, and the biggest impediments to them hitting their KPIs include X, Y, and Z. Currently they are using products from companies A, B, and C, but those products don’t allow them to do these three critical things…”

Also, there’s nobody you know more intimately than yourself. That is why so many great businesses have been formed from personal need.

6. You know the market

In almost all cases, there are several people already devoting their lives to your idea. In order to win, you need to engulf yourself into your market in order to have the requisite insight and vision needed to win. Chris Dixon (Andreessen Horowitz) has said that you need to devote at least 10,000 hours on your market to get this insight — whether by working in the market, living the problem (ex. being a social media addict who then starts a social media company), and/or devoting that time towards research.

If you are not an expert on your market, then it’s time to get to work. There are no shortcuts here.

7. Sufficiently large market

Large and fast growing markets have the power to pull mediocre companies into greatness, and conversely, dying markets can pull otherwise solid companies into the ground. If you are going to devote your life to an idea, the market where you operate better be big enough (or growing at such a fast rate) to support a meaningful and enduring company.

Any market with less than 10 million people or multiple billions in annual revenue that is not growing at a very fast rate will be very hard to address, and is probably not worth your time. For example, even if you were lucky enough to be moderately successful in a $500 million market, you would likely still only have around a $50 million business.

You will die winning a small market, so be smart and don’t start your company in a graveyard.

8. Original secret sauce

Every great business has a secret sauce. Given, not every company starts out with that secret sauce, but building a company without a plan for how you will differentiate and win from the outset is simply foolish.

Also, your secret sauce needs to be original. If it’s obvious, that is almost always a bad sign. The best ideas have a secret sauce that is transformational, not incremental.

What secret do you know that will help you win? For example, Tony Hsieh started Zappos with a very distinct insight and secret sauce — customer service. His transformational insight was that buying shoes online was really a customer service problem, and not a retail problem.

9. You have tried to kill your idea

It is very easy to fall in love with your idea — after all, it’s your baby, and almost nobody will tell you your baby is ugly. Positive reinforcements are very easy to find.

Your job in the idea stage is to find the things that make your idea bad. Try to kill your idea, and then, one-by-one, iterate and eliminate the negative aspects of the idea. The result will be a much more defensible foundation by which to start.

10. You are sharing your idea!

Nobody is going to steal your idea. Think about it — do you really think your idea is so great, so original, that somebody who hears it is going to go home, quit their job, and devote their entire lives to it? And be successful? The chances are near zero.

You need to be pitching your idea all day long to anybody who will listen, and incorporating all the feedback you receive into improving the idea. Feedback is an entrepreneur’s best friend, and Silicon Valley entrepreneurs understand this better than anybody else. For example, on any given night, you can find 20 different events in Silicon Valley where people are openly sharing their ideas, and it is this collaborative, teamwork-oriented culture that leads to innovation.

Perfecting Your One Sentence Pitch

As a startup founder, you will pitch your business thousands of times to potential customers, partners, team members, investors, and more.

As a startup founder, you will pitch your business thousands of times to potential customers, partners, team members, investors, and more.

When you pitch, you need to grab the listener's attention quickly, and communicate all of the core elements of your idea in a clear and concise manner. The goal is to get so good at pitching your business that could do your one sentence elevator pitch, in the short amount of time it takes to ride an elevator (perhaps with someone influential). In order to do this, I recommend using the simple Founder Institute one sentence pitch format described below.

Remember: If you can't describe your business in one sentence, then you don't understand it well enough.

The Founder Institute's Best One Sentence Pitch Format

Let's go through each of the items;

The "defined offering" needs to be short, simple and capable of being understood by everyone, like "a website," "a mobile application," "hardware," or "desktop software."

The "defined audience" is the initial group of people that you will market your offering to. In the case of consumer applications, it is usually a demographic, such as "women age 25 to 35 years old." In the case of business applications, it is usually a job function at a type of corporation, such as "system administrators at medium sized technology businesses."

Now that you have an offering helping an audience, you need to "solve a problem." The problem needs to be something that everyone understands, such as "reduce the time collecting bill payments" or "engage in an immersive entertainment experience."

The final component, the "secret sauce," adds your unique approach to solving the problem and demonstrates a mastery of the market. Some examples are "by sending automated email alerts based on analysis of highest response times" or "with virtual worlds constructed in reaction to the movements of the players."

Here are some more pointers; First, avoid using adjectives, particularly superlatives. Never say "first," "only," "huge" or "best," as these words signal inexperience. Second, properly define your target market. For example, "women" or "small businesses" are way too large and not nearly targeted enough. Third, eliminate any buzzwords, acronyms or industry jargon from your pitch. Finally, keep it short. It's easy to write a long sentence, but the right thing is to be concise.

In the short video below, Adeo Ressi, Founder & CEO of the Founder Institute, explains Startup Madlibs in full:

The Incredible History of Buffalo, New York In 5 Minutes

43 North, the world's largest business idea competition, has released an awesome new video chronicling the amazing history of Buffalo NY.

43 North, the world's largest business idea competition, has released an awesome new video chronicling the amazing history of Buffalo, New York. The video titled "Next Things Now: Innovation & Entrepreneurship in Buffalo" summarizes all that Buffalo’s history has given to the world and as well as a hint of whats possible in the new era of One Buffalo. Check it out below:

Co-authored by The Herd Report